Will Mortgage Rates Drop in 2026? What Markets Say

The question everyone with a home on their radar is asking right now: will mortgage rates drop in 2026 enough to matter? After the brutal repricing of 2022 and 2023, rates have come off their peak, but they have not delivered the relief millions of sidelined buyers and locked-in homeowners were banking on.

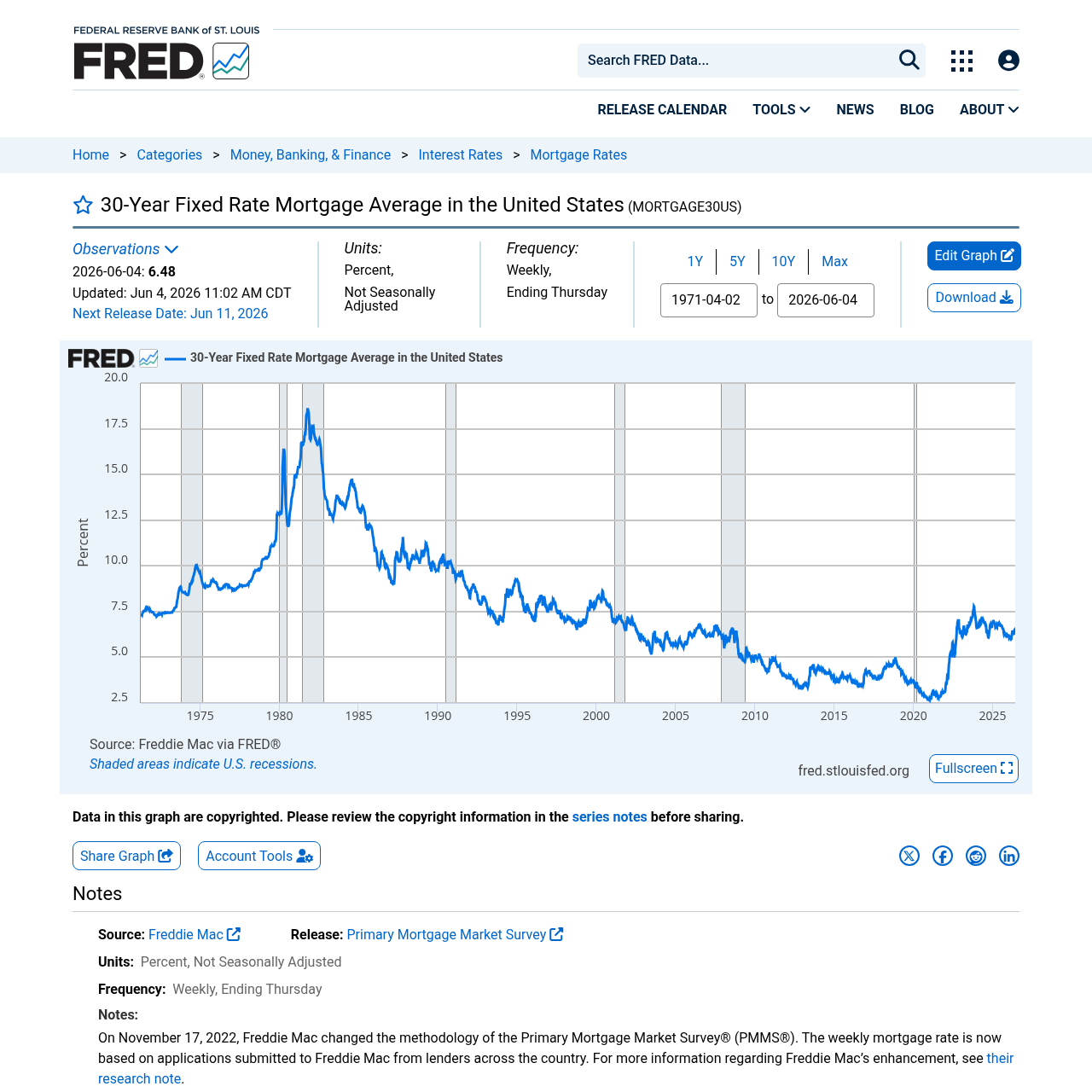

As of the first week of June 2026, the 30-year fixed sits at 6.48% according to Freddie Mac's Primary Mortgage Market Survey. That is better than the 6.85% recorded a year ago. It is nowhere near the sub-3% era. For a $400,000 mortgage, the difference between 6.5% and 5.5% is roughly $250 a month. The stakes are real.

We track the live Fed-rate prediction markets at MacroOdds precisely because the bond market -- and therefore the mortgage market -- prices in Fed policy expectations weeks and months before any actual decision. Right now those markets are telling a cautious story. Here is what the data, the forecasts, and the odds actually say.

Where Mortgage Rates Stand Heading Into Mid-2026

Freddie Mac's weekly survey, which feeds directly into the FRED MORTGAGE30US series, shows the 30-year fixed averaging 6.48% for the week ending June 4, 2026. The week prior it was 6.53%. Five weeks ago it touched 6.36%. The trend is a slow, choppy drift lower -- not the decisive break buyers are hoping for.

For context, the 30-year rate peaked near 7.8% in late 2023. The relief since then has been real but modest. A borrower who waited from that peak to today has saved roughly 130 basis points. A borrower who waited expecting a return to 4% or 5% is still waiting.

The 15-year fixed, which matters for refinancers and shorter-horizon buyers, stood at 5.79% the same week. Both rates moved in near lockstep with the 10-year Treasury yield over that same period -- exactly as the mechanics of mortgage pricing predict.

Do Fed Rate Cuts Actually Lower Mortgage Rates?

This is the single most misunderstood point in all of housing finance. The Fed funds rate does not directly set your mortgage rate. The Fed controls overnight lending between banks. Your 30-year mortgage is priced off the 10-year Treasury yield, which is set by global bond markets, not by Jerome Powell or Kevin Warsh.

That said, the Fed is not irrelevant. When the Fed signals rate cuts, bond investors anticipate lower future short-term rates, which can pull long-term yields down as well. The problem is that this transmission is indirect, slow, and often already priced in by the time the Fed actually acts. The bond market leads; the Fed follows.

The typical spread between the 10-year Treasury yield and the 30-year mortgage rate runs 150 to 200 basis points in normal times. During the 2022-2024 stress period, that spread blew out to nearly 300 basis points as lenders demanded extra compensation for prepayment risk and market volatility. As of mid-2026, the spread has compressed but remains above its long-run average. That overhang represents potential mortgage rate relief that could materialize even without any Fed action, simply as the bond market normalizes.

| Rate / Yield | Level (June 2026) | Notes |

|---|---|---|

| 30-year fixed mortgage | 6.48% | Freddie Mac PMMS, week of June 4 |

| 15-year fixed mortgage | 5.79% | Freddie Mac PMMS, week of June 4 |

| 10-year Treasury yield | ~4.4% | Approximate, mid-2026 trading range |

| Fed funds rate (target) | 4.25% - 4.50% | Unchanged since late 2024 |

| Mortgage-to-Treasury spread | ~200+ bps | Still above the 150-170 bps historical norm |

Key rate reference points as of early June 2026. Sources: Freddie Mac, FRED, U.S. Treasury.

The bottom line: a Fed cut helps at the margin, mostly by giving bond investors confidence that rates are moving in one direction. But the 10-year yield can fall on its own if inflation cools, growth slows, or foreign demand for Treasuries picks up. Mortgage borrowers who anchor their timing entirely to Fed meeting dates are watching the wrong clock.

2026 Mortgage Rate Predictions From Major Institutions

The three institutions that produce the most widely-followed mortgage rate prediction 2026 forecasts are Fannie Mae, the Mortgage Bankers Association, and Freddie Mac's own research team. Their current views bracket a fairly narrow band -- and that narrow band tells its own story.

| Institution | Q4 2026 Forecast | Key Assumption | Direction |

|---|---|---|---|

| Fannie Mae (ESR Group) | 5.9% | Inflation cools to ~2.5%; 1-2 Fed cuts materialize in H2 | Down ~60 bps from current |

| Mortgage Bankers Association | 6.4% | Sticky inflation; Fed holds through year-end | Roughly flat |

| Freddie Mac Research | ~6.2% | Gradual Treasury yield compression; no dramatic Fed shift | Modest decline |

| Consensus (average) | ~6.2% | Base case assumes limited Fed action | Down 25-30 bps |

2026 year-end 30-year fixed-rate mortgage forecasts from major housing finance institutions. Forecasts current as of mid-2026.

Fannie Mae's September 2025 press release was the most optimistic of the major forecasters, projecting rates end the year at 5.9%. Their scenario requires inflation to fall meaningfully toward the Fed's 2% target and for at least one or two rate cuts to materialize. That was their base case in September 2025. Given the inflation data since then -- April 2026 CPI running at 3.8% year-over-year -- that forecast looks increasingly optimistic.

The MBA's view is more conservative: rates stay near 6.4% through year-end. That scenario reflects persistent inflation keeping the Fed on hold and the 10-year yield anchored above 4%. For buyers hoping to time the market, the MBA's forecast is the more painful one -- it says the window you are waiting for may not open in 2026.

What Prediction Markets Say About Fed Cuts and Mortgage Direction

This is where MacroOdds adds a dimension that the standard housing forecasts miss. Prediction markets aggregate the real-money views of thousands of traders who have skin in the game. They are not a crystal ball, but they are the most efficient forward read available on the probability of near-term Fed action.

As of early June 2026, Polymarket's "How many Fed rate cuts in 2026?" market -- which has cleared over $21 million in volume -- is pricing roughly a 75% probability of zero cuts for the full calendar year. Kalshi's equivalent market shows similar numbers. For the June 17 FOMC meeting specifically, no-change odds were running at 98%+.

The implication for mortgage rates is direct. If markets believe the Fed will not cut at all in 2026, the 10-year Treasury yield has limited downside in the near term. That caps how far mortgage rates can fall. The optimistic Fannie Mae scenario (5.9% by year-end) essentially requires the market's consensus to shift significantly -- for traders to start pricing in 1-2 cuts -- before rates can break much lower.

You can watch the live probability shifts on our Fed rate cut probability page and our mortgage rate prediction tracker. When those odds move, mortgage rates tend to follow within days, not weeks.

When Will Mortgage Rates Drop Meaningfully?

"Meaningfully" is doing a lot of work in that question. A 25 or 50 basis point drift is meaningful for a monthly payment calculation but it may not be the psychological unlock that brings sidelined buyers back in volume. Most housing economists put the unlocking threshold somewhere around 5.5% to 5.75%, where affordability math starts to work again for median-income buyers in mid-tier markets.

Getting to 5.5% from 6.5% requires roughly 100 basis points of decline. At the current pace -- the 30-year has shed about 37 bps year-over-year -- that is a three-year journey at best, absent a significant macro shock that accelerates Fed cuts. A recession, a sharp drop in inflation, or a financial stability event could compress that timeline. None of those are the scenario anyone should be rooting for.

The more actionable framing: rates are more likely to drift gradually lower than to plunge. If you are a buyer waiting for 5%, you are probably waiting until 2027 at the earliest under any plausible base case. If you can underwrite a purchase at current rates and plan to refinance when rates fall, the math is different. The recession odds page on MacroOdds gives you one more data point for thinking through that timeline risk.

How Low Will Mortgage Rates Go in 2026 and Beyond?

The range of reasonable outcomes for year-end 2026 runs from roughly 5.9% (Fannie Mae's bull case, requiring Fed cuts and inflation cooling) to 6.5%+ (the MBA's bear case, requiring inflation to stay sticky). That 60-basis-point spread reflects genuine macro uncertainty, not forecaster sloppiness.

Beyond 2026, the structural view matters more than the cyclical one. The neutral rate -- the theoretical Fed funds rate that neither stimulates nor restrains the economy -- is broadly estimated to be higher now than it was in the 2010s. Many Fed officials and market economists place it at 3% to 3.5%, compared to the near-zero estimate that dominated the post-2008 decade. A higher neutral rate means the long-run floor for the 10-year Treasury is also higher, which means the long-run floor for mortgages is higher.

The sub-3% mortgage rates of 2020-2021 were a historic anomaly driven by zero policy rates and aggressive Fed balance sheet expansion. We should not use them as our mental baseline for "normal." A world where mortgage rates eventually settle around 5.5% to 6% would actually be close to the 30-year historical average. It would feel like a relief from today but it would not be the return to 2021.

What This Means for Homebuyers, Refinancers, and Investors

For first-time buyers, the calculus comes down to whether you can afford the monthly payment today and whether your income and job security support a long-term commitment. Rates at 6.5% are painful but they are not historically extreme. If you find a home that works at current rates, waiting for 5% could mean waiting two to three years and competing with a rush of demand when rates eventually fall.

For existing homeowners sitting on sub-4% rates, the lock-in effect remains real. Refinancing does not make financial sense unless your personal situation has changed (cash-out need, shorter term, ARM reset) or rates fall below roughly 5.75% to 6%. Keep an eye on our Fed rate cut probability page -- a shift in the market's cut expectations often leads a meaningful Treasury rally by several weeks.

For real estate investors, the spread between cap rates and mortgage rates matters more than the absolute level. In many markets, that spread is still compressed, which means investment math is tight. A 50-basis-point rate move alone rarely changes the investment case. Rental growth and local supply dynamics are doing more work in the 2026 investment calculus.

All three groups benefit from watching when the Fed will cut rates -- because the first credible signal of a cut cycle, even before the first actual cut, tends to move Treasury yields and mortgage rates. The signal matters as much as the action.

The Fed-to-Treasury-to-Mortgage Chain: A Practical Guide

We talk about this chain abstractly, but it is worth making it concrete. Here is the sequence that actually moves your mortgage rate:

- Inflation and jobs data shift -- a weaker CPI print or a rising unemployment rate gives traders confidence the Fed will cut sooner.

- Bond investors buy 10-year Treasuries in anticipation of lower future short-term rates, pushing the 10-year yield down.

- Mortgage-backed security (MBS) spreads tighten as investor appetite for yield improves, further compressing the mortgage-to-Treasury premium.

- Lenders pass through the lower benchmark and tighter spreads in the form of lower quoted mortgage rates -- usually within days of a significant Treasury move.

- The Fed eventually cuts the funds rate, which can reinforce the move but rarely drives it. By that point, the mortgage market has already priced in most of the benefit.

This is why prediction markets are a useful leading indicator for mortgage direction. They aggregate trader beliefs about the first three steps in that chain in real time. When the Polymarket odds for a Fed cut in a given quarter tick up from 20% to 50%, the Treasury market has usually already started moving. Watching those odds at MacroOdds gives you a head start on the conventional calendar-watching approach.

The Spread Opportunity Nobody Talks About

There is a nuanced tailwind for mortgage rates that gets far less attention than Fed meeting speculation: spread compression. As we noted above, the spread between the 10-year Treasury yield and the 30-year mortgage rate blew out to nearly 300 basis points at the height of the 2022-2023 stress period. The historical norm is closer to 150-175 basis points.

That extra 100-125 basis points of premium reflected lender caution, MBS market illiquidity during the Fed's quantitative tightening program, and elevated prepayment risk uncertainty. As those conditions normalize -- as the Fed slows or stops its balance sheet runoff, as MBS markets find better liquidity -- the spread can compress back toward historical levels even with no change in the 10-year Treasury yield itself.

What that means in practice: the path from 6.5% to 5.75% might not require the 10-year to fall by a full 75 basis points. It might require the 10-year to fall 40 basis points and the mortgage spread to compress another 35 basis points. Two forces moving together is faster than one moving alone. This is part of why Fannie Mae's 5.9% year-end forecast is not crazy even if Fed cuts do not materialize.

The Recession Wildcard and Mortgage Rates

There is one scenario where mortgage rates fall faster than any forecast assumes: a recession. In a recession, the Fed cuts aggressively, Treasury yields fall sharply, and mortgage rates follow. The 2008-2009 experience saw the 30-year fixed fall from above 6% to near 5% in roughly six months as the Fed slashed rates and launched QE.

But this is not the scenario to root for. A recession that causes mortgage rates to fall also tends to cause unemployment to rise, home prices to fall in some markets, lending standards to tighten, and consumer confidence to crater. Lower rates during a recession do not necessarily create a buyer's paradise -- they create a buyer's paralysis.

You can track real-money recession probability estimates on our recession odds page. As of mid-2026, markets are pricing a moderate but not alarming probability of recession in the next 12 months. The base case remains a slow-growth, sticky-inflation environment -- the kind that keeps mortgage rates frustratingly elevated without providing the macro shock that breaks them dramatically lower.

The Bottom Line: Calibrated Patience, Not Blind Waiting

Will mortgage rates drop in 2026? Almost certainly, yes -- but probably by less than most buyers are hoping for. The institutional consensus clusters around a year-end 30-year rate of 6.0% to 6.4%, with the optimistic bull case at 5.9% requiring inflation to cooperate and the Fed to eventually move. Prediction markets currently assign a 75% probability to zero Fed cuts this year, which keeps the bull case firmly in the minority.

The actionable takeaway is not "wait" or "don't wait" -- it is to stop treating mortgage rates as a binary event (high now, low later) and start treating them as a continuous market variable that you can track in real time. The bond market signals a rate shift before it shows up in lender quotes. Prediction markets signal a policy shift before the Fed announces it.

MacroOdds is built precisely for this kind of intelligence. Follow the mortgage rate prediction page, the Fed rate cut probability tracker, and the when will the Fed cut rates analysis to stay ahead of the noise. When the data changes, we will tell you -- and you will see it in the odds before you see it in the headlines.

Frequently asked questions

Will mortgage rates drop in 2026?

The consensus from major forecasters is yes, but modestly. Fannie Mae expects the 30-year fixed to end 2026 near 5.9%, while the MBA's more conservative forecast holds rates near 6.4%. The actual outcome depends heavily on whether inflation falls toward 2% and whether the Fed cuts rates at all this year. Prediction markets currently assign about a 75% probability to zero Fed cuts in 2026, which supports the more cautious forecasts.

Does a Fed rate cut lower my mortgage rate?

Not directly. Your 30-year fixed mortgage rate is priced off the 10-year Treasury yield, not the Fed funds rate. A Fed cut can lower mortgage rates indirectly by signaling lower future short-term rates, which pulls Treasury yields down. But the bond market typically prices in expected Fed cuts weeks or months before the actual decision -- meaning rates may fall before the Fed acts, and see little additional movement after.

When will mortgage rates hit 5%?

Under the current base case, probably not until 2027 or later. Getting from the current 6.48% to 5% requires roughly 150 basis points of decline. At the pace of the past year (about 37 bps of annual improvement), that is a multi-year journey. A recession or significantly faster-than-expected inflation decline could accelerate the timeline, but neither is the base case as of mid-2026.

Why do mortgage rates follow the 10-year Treasury instead of the Fed?

Because mortgage lenders need a benchmark with a duration that matches the average time a borrower keeps a mortgage -- roughly 7 to 10 years. The 10-year Treasury yield reflects the market's long-run view on inflation and growth, which is the same view baked into a fixed mortgage rate. The Fed funds rate is an overnight rate and reflects very short-term monetary conditions, which are less relevant for a 30-year commitment.

What are prediction markets saying about mortgage rates?

Prediction markets like Polymarket and Kalshi don't have direct mortgage-rate contracts, but their Fed-cut probability markets are a strong leading indicator. As of June 2026, those markets show roughly 75% odds of zero Fed cuts in 2026. Since mortgage rates are downstream of Fed expectations, this implies limited downside for rates in the near term -- absent a major change in inflation or economic data.

Should I buy a home now or wait for lower rates?

That depends on your personal financial situation, not just rates. If you can afford the monthly payment at current rates and plan to stay long-term, waiting for lower rates carries opportunity costs (continued rent payments, potential home price appreciation). If current rates would stretch your budget to the breaking point, waiting for better affordability is prudent. The common advice from housing economists: "marry the house, date the rate" -- buy if the fundamentals work, and refinance when rates fall.

How does the mortgage-to-Treasury spread affect rates?

The spread between the 10-year Treasury yield and the 30-year mortgage rate is normally around 150-175 basis points. During 2022-2024, it blew out to nearly 300 basis points due to MBS market stress and Fed balance sheet uncertainty. As that spread normalizes back toward historical levels, mortgage rates can fall even without the 10-year Treasury yield moving. This "spread compression" effect is one reason rates could improve more than the headline Fed-cut story implies.

What is the 2026 mortgage rate forecast from Fannie Mae?

Fannie Mae's Economic and Strategic Research Group forecast (published September 2025) projects the 30-year fixed-rate mortgage will average 5.9% by the fourth quarter of 2026. This is the most optimistic among major institutional forecasters and assumes inflation moderates toward 2% and the Fed makes at least one or two rate cuts in the second half of the year.